The gap between listing price and true cost

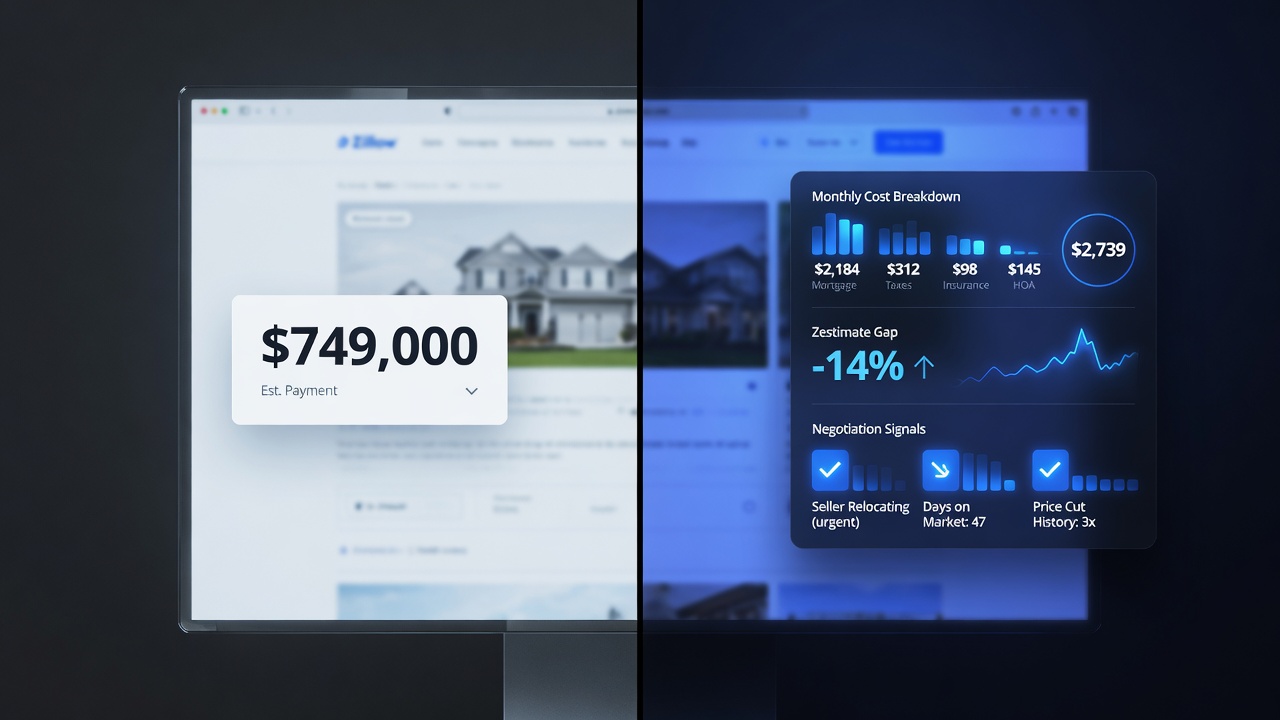

The most important number in a home purchase isn't the listing price — it's your monthly payment. And your monthly payment is not the mortgage. It's the mortgage plus property tax, homeowner's insurance, HOA fees, PMI (if your down payment is under 20%), and a maintenance reserve. First-time buyers frequently forget several of these.

On a $650,000 home at 6.8% with 10% down, the mortgage payment is roughly $3,820/month. Add property tax at 1.1% ($596/month), insurance at 0.65% ($352/month), PMI at 0.8% ($433/month), and a 1% maintenance reserve ($542/month) — and your actual monthly cost is closer to $5,743. Zillow shows you $3,820.

That gap — between the mortgage payment and the full cost — is where budgets break and buyers get into homes they can't comfortably afford.

What the Zestimate is actually telling you

Zillow shows the Zestimate on every listing, but most buyers don't know how to read it. The Zestimate is Zillow's automated valuation model — a computer estimate of market value based on comparable sales, tax records, and listing data. It's not appraisal-grade, but it's a useful first signal.

What matters is the gap between the list price and the Zestimate, expressed as a percentage:

- Listed 5–10% above Zestimate: Normal range. Sellers typically price slightly above automated estimates to leave negotiation room.

- Listed 10–20% above Zestimate: Seller is aggressive or the property has features Zillow can't capture (renovated kitchen, better lot). Worth investigating before offering.

- Listed at or below Zestimate: Motivated seller, estate sale, quick close needed, or the property has issues the Zestimate didn't penalize it for. Negotiate accordingly.

Zillow shows both numbers side by side, but it doesn't calculate the gap for you or tell you what it means. That's the first calculation any serious buyer should make.

| Listing Status | Median Error Rate | Implication |

|---|---|---|

| On-market listing | ~2.4% | Most accurate; Zillow has MLS data |

| Off-market home | ~7.5% | Use only as rough estimate; +/-$50K on $700K home |

| Recently sold (< 3 months) | ~3.0% | Reliable anchor; compare to final sale price |

| Unique/luxury property | 10–20%+ | Comps are scarce; Zestimate unreliable |

| New construction | 5–12% | No sales history; estimate based on neighborhood only |

| Major renovation done | 8–15% | Zillow can't see unreported upgrades |

Days on market: the signal most buyers ignore

Days on market (DOM) is the most underused data point on any listing. It tells you how long the property has been available at its current price — and that tells you a lot about seller motivation.

- 0–7 days: Fresh listing, competitive market. Full-price offers are common. Contingencies may cost you the deal.

- 8–30 days: Normal range. Room to negotiate exists, especially if there are no competing offers.

- 31–60 days: Seller has had limited interest. Now is the time to anchor below asking. Ask your agent to find out why it's sitting.

- 60+ days: Significant leverage. Price reduction requests are routine. The seller is likely frustrated — use that in your negotiation.

Zillow shows DOM, but it doesn't interpret it for you relative to the local market average, and it doesn't tell you whether the listing has been relisted (resetting the counter artificially). Always check the price history tab — if the same property appeared at a higher price 90 days ago and relisted, the true DOM is much longer than shown.

What closing costs actually are (and why Zillow doesn't show them)

Closing costs are the fees paid at the end of a real estate transaction, in addition to the down payment. They typically run 2–5% of the purchase price. On a $650,000 home, that's $13,000–$32,500 — due at closing, on top of your down payment.

Zillow doesn't show closing costs because they vary by location, lender, and transaction structure. But the major categories are consistent:

- Lender fees: Origination, underwriting, and processing. Typically $1,000–$3,000.

- Title insurance: Owner's and lender's policy. Typically $1,000–$2,500.

- Escrow/attorney fees: $800–$2,000 depending on state.

- Prepaid interest: Interest from closing date to end of month. Varies by closing date and loan size.

- Property tax escrow: 2–3 months of property tax upfront into escrow.

- Homeowner's insurance: First year's premium, due at closing.

- Recording fees: County fee to record the deed. Typically $100–$300.

Most buyers don't learn these numbers until they receive the Closing Disclosure 3 days before signing. By then, it's too late to adjust your budget. Budget for closing costs from the day you start seriously shopping.

Seller equity: why it matters for your offer

One piece of data Zillow doesn't surface is the seller's approximate equity position — how much they owe versus what the property is worth. This matters because equity constrains how much a seller can negotiate.

A seller with significant equity (they bought 10 years ago, property has appreciated) has room to come down. They can accept a lower offer and still net a meaningful amount after paying off their mortgage and covering closing costs. A seller who bought recently at near-current prices has very little room — they may not be able to accept a below-ask offer without coming out of pocket at closing.

You can estimate seller equity from public tax records — purchase date, original purchase price, and current Zestimate. It's not always accurate, but it tells you whether negotiating hard is worth attempting.

How to look at a Zillow listing like an experienced buyer

Calculate the true monthly cost first

Before you look at the photos, calculate the full monthly cost at your target down payment and current rates. If the number doesn't work in your budget, move on — no amount of loving the kitchen changes what you can afford.

Check the price vs. Zestimate gap

Calculate the percentage difference. Anything over 10% above Zestimate warrants a closer look at why the seller believes the premium is justified.

Read the price history

Check how many times the property has been listed, at what prices, and whether the counter has been reset by relisting. The real DOM is the most important negotiation signal on the page.

Budget for closing costs before you fall in love

Estimate 3–4% of the purchase price as closing costs and make sure you have that in addition to your down payment before you tour.

See all of this on every Zillow listing — automatically

HomePilot calculates true monthly cost, price vs. Zestimate gap, deal score, closing cost estimate, and seller equity in the side panel while you browse. Free for 5 listings per month.

Add HomePilot to Chrome — Free →5 free analyses/month · Works on Zillow, Redfin & Realtor.com