Why the listing calculator lies to you

Every major listing site — Zillow, Redfin, Realtor.com — shows you a "monthly payment" estimate. That number is typically just principal and interest on the mortgage. Sometimes it includes property tax and insurance. Almost never does it include HOA fees, PMI, or maintenance reserves.

The gap between the listing calculator's number and your actual monthly obligation is usually $300–$700 per month on a median-priced home. On a $600,000 home with a 10% down payment, it can be $800+ more than the advertised payment. That difference compounds over the life of your ownership — and it's the difference between a home that fits your budget and one that slowly squeezes it.

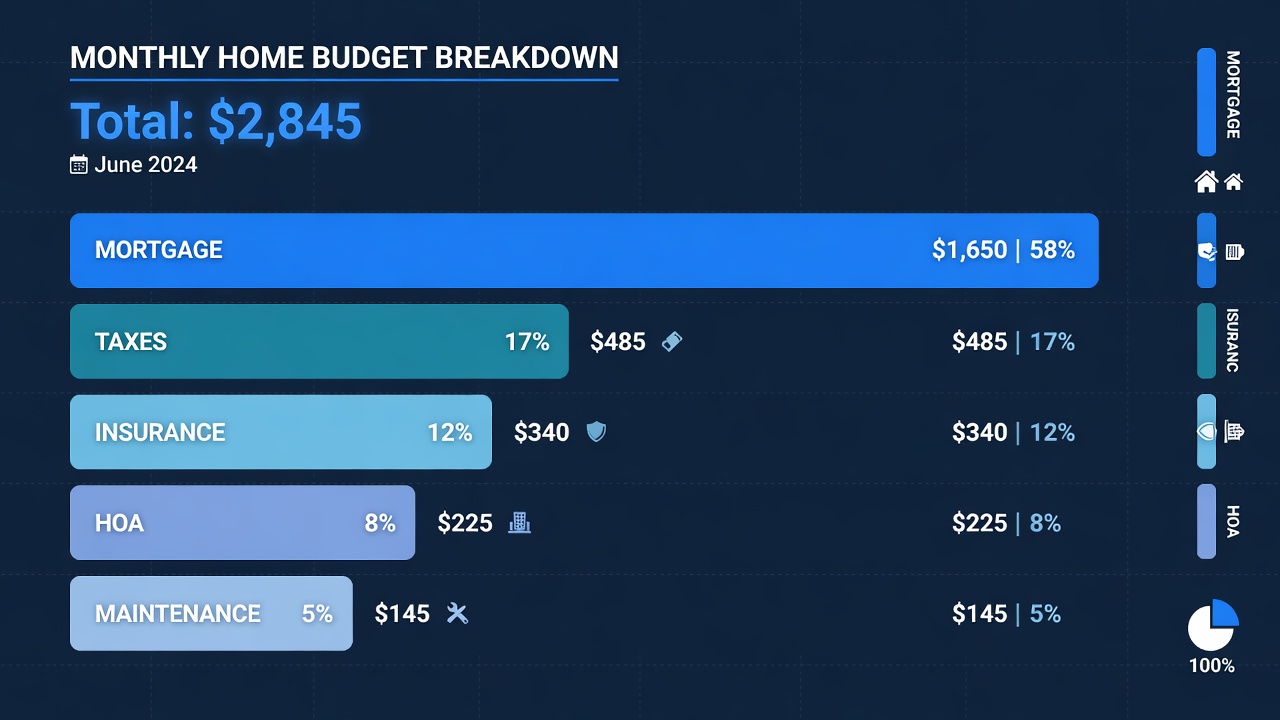

Every line item in your true monthly cost

Principal and interest (P&I)

This is the base mortgage payment — the loan amount amortized over your term at your interest rate. It's the number listing sites show you. On a $540,000 loan (10% down on a $600K home) at a 6.75% rate, 30-year fixed, this is approximately $3,502/month.

Property tax

Listed as an annual figure on most listings, but it hits monthly as part of your escrow payment. Property taxes vary dramatically by state and county — from under 0.5% in Hawaii and Alabama to over 2% in New Jersey and Illinois. On the same $600K home, your monthly tax escrow could be anywhere from $250 to $1,000+ depending on location. HomePilot pulls the actual property tax from the listing data.

Homeowner's insurance (HOI)

Also paid via escrow monthly. National average is roughly 0.5–1% of home value annually — $250–$500/month on a $600K home. Higher in coastal, flood-prone, or wildfire-risk areas. Don't assume the low end; get a real quote for the property before closing.

PMI (Private Mortgage Insurance)

Required on conventional loans when your down payment is under 20%. PMI typically costs 0.5–1.5% of the loan amount annually — on a $540K loan, that's $225–$675/month. PMI drops off once you reach 20% equity, but it's a real cost until then. With a 10% down payment, you'll pay PMI for several years.

HOA fees

For condos, townhomes, and many planned communities, HOA fees are mandatory and can range from $100/month to $1,500+/month for high-rise buildings with amenities. This number is on the listing but often not factored into the monthly payment estimate. For condos in major cities, HOA fees frequently exceed the property tax payment.

Maintenance reserve

The cost most buyers forget entirely. A standard rule of thumb is 1% of the home's value per year in maintenance — roof, HVAC, appliances, plumbing, exterior. On a $600K home, that's $6,000/year, or $500/month. This doesn't come as a monthly bill — it comes as a periodic large expense — but budgeting for it monthly is what prevents a furnace replacement from becoming a financial crisis.

| Cost Item | How to Calculate | Typical Range |

|---|---|---|

| Mortgage (P+I) | Loan amount × monthly rate factor | Largest component; fixed for 30yr |

| Property tax | (Purchase price × tax rate) ÷ 12 | 0.5–2.5% of value/year |

| Homeowner's insurance | Annual premium ÷ 12 | $80–$200/month |

| PMI (if < 20% down) | 0.5–1.5% of loan/year ÷ 12 | $100–$400/month |

| HOA fees | Fixed monthly | $0–$500+/month |

| Maintenance reserve | 1–2% of home value/year ÷ 12 | $300–$800/month |

| Utilities estimate | Based on home size + climate | $200–$600/month |

| Total true monthly cost | Sum of all above | Often 40–60% more than mortgage alone |

What income do you need?

Lenders typically use a 28/36 rule: your PITI payment should be under 28% of gross monthly income, and all debt payments (including student loans and car payments) should be under 36%. If your full PITI on a $600K home is $4,800/month, the 28% front-end ratio requires roughly $17,150/month ($205,800/year) in gross income.

HomePilot calculates the income required for the exact listing you're looking at, based on your specific down payment and the property's tax and HOA data. This tells you before you visit whether the home is actually in your financial range — not just whether you like it.

Using HomePilot to see the real number

Open any Zillow, Redfin, or Realtor.com listing

HomePilot detects the listing price, property tax, HOA fees, and Zestimate automatically. No copy-pasting or form filling.

Enter your down payment and interest rate

Input your down payment percentage and the current rate you've been quoted (or the current market rate). HomePilot calculates your PMI tier and loan amount from these.

Read the full PITI+ breakdown

HomePilot shows every component itemized — P&I, tax, insurance, PMI (if applicable), HOA, and maintenance reserve — plus the total and the income required to qualify. This is the number to compare across homes you're considering.