Get pre-approved — not pre-qualified

Before you make an offer on any home, you need a pre-approval letter from a lender. This is non-negotiable in most markets. Sellers routinely reject offers that arrive without one, and in competitive markets, listing agents will screen them out before even presenting them.

The distinction between pre-approval and pre-qualification matters more than most buyers realize:

- Pre-qualification is a rough estimate based on self-reported income and debt. No documents are verified. It takes 10 minutes, means almost nothing to a seller, and is often confused for something more credible than it is.

- Pre-approval is a conditional commitment from a lender based on verified income, assets, employment history, and a hard credit pull. The lender has actually reviewed your financial picture and confirmed, subject to property appraisal, that they will lend you the stated amount.

Only pre-approval is credible to sellers. Get it before you start serious home tours, not after you find a home you want. The process typically takes 1–3 business days and requires:

- W-2s or 1099s from the last 2 years (plus tax returns if self-employed)

- Recent pay stubs (most recent 30 days)

- Bank and investment account statements (2–3 months)

- A hard credit inquiry (this will slightly lower your score temporarily — it's normal)

Your pre-approval letter will state a maximum loan amount. That number does not mean you should offer that much. It means the bank will lend you up to that much. Whether you can actually afford the monthly cost is a separate calculation — which is step 2.

Calculate the true monthly cost before you fall in love

Offer price is not the same as what you can afford. The offer price determines your loan amount, which determines your mortgage payment — but your mortgage payment is only one component of your actual monthly cost.

Your true monthly cost includes all of the following:

- Principal and interest (P&I): The core mortgage payment, determined by your loan amount, interest rate, and loan term

- Property tax: Use the actual tax figure from the county assessor or the listing, not an estimate. Property tax varies dramatically by state and municipality — from under 0.5% in some states to over 2% in others

- Homeowner's insurance: Typically $100–$250/month depending on home value and location. Higher in flood-prone or wildfire-adjacent areas

- HOA fees: Shown on the listing — but often not counted by buyers. A $400/month HOA fee on a condo adds $4,800 per year to your cost

- PMI (private mortgage insurance): Required if your down payment is under 20%. Typically 0.5–1.2% of the loan amount annually. On a $500,000 loan, PMI at 0.8% is $333/month

- Maintenance reserve: The industry standard is 1% of the home's value per year. On a $550,000 home, that's $458/month you should budget for repairs, appliance replacements, and upkeep — whether or not you spend it every month

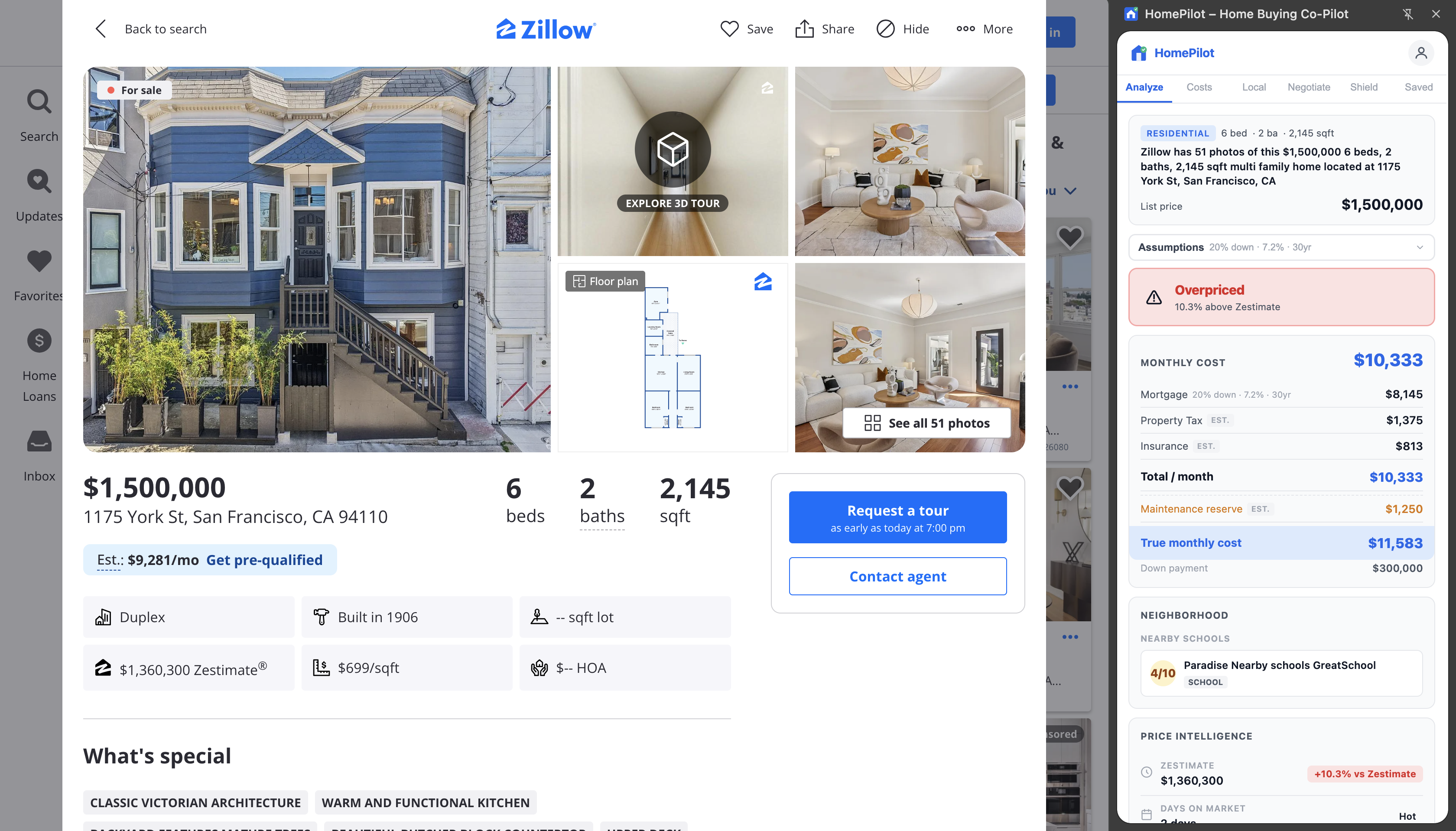

P&I: $3,454 · Property tax (1.2%): $575 · Insurance (0.7%): $335 · PMI (0.85%): $384 · Maintenance (1%): $479

True monthly cost: $5,227. Zillow shows $3,454.

The gap between what mortgage calculators show and what you actually pay every month can be $1,500–$2,000 on a typical home. Run this calculation first — before you tour, before you're emotionally invested — so you know what offer price range is genuinely within your budget.

HomePilot calculates this automatically in the side panel on every Zillow, Redfin, and Realtor.com listing. You see the full monthly cost breakdown before you schedule a tour.

Read the negotiation signals

Before you decide what to offer, you need to understand the seller's position. Three data points give you most of what you need:

| Days on Market | Market Signal | Suggested Offer | Contingencies |

|---|---|---|---|

| 0–7 days | High demand | At list price or 1–2% above | Keep all; minimize asks |

| 7–14 days | Normal demand | At list price | Standard inspection + financing |

| 14–30 days | Moderate interest | 1–3% below list | All contingencies |

| 30–60 days | Seller may be motivated | 3–7% below list | All contingencies + closing cost credit |

| 60–90 days | Seller likely motivated | 5–10% below list | Full contingencies; request repairs |

| 90+ days | High seller motivation | 8–15% below list | Negotiate everything; price, repairs, credits |

Days on market (DOM)

DOM is the most underused negotiation signal in real estate. Every 30 days a home sits unsold, the seller gets more motivated. A listing at 60 DOM with no accepted offer has had months of showings, feedback, and presumably no takers at that price. That's leverage you can use.

The key nuance: check whether the listing was relisted. A home that was listed for 90 days, pulled, and then relisted will show a low DOM on Zillow — but the actual market exposure is much longer. Check the price history tab on every listing to see the full timeline.

- 0–14 days: Fresh listing. Seller has no urgency. Your offer needs to be competitive.

- 15–45 days: Some market feedback. If priced above Zestimate, you have room to negotiate.

- 45–90 days: Seller has likely received offers they rejected, or no offers at all. Meaningful negotiation room.

- 90+ days: Something is keeping buyers away — price, condition, location, or all three. Investigate before you bid, but if the issue is solvable, your leverage is significant.

Price history

A home that dropped $25,000 in three months tells you the seller started too high and has already capitulated once. They may be willing to come down further. A home with no price changes that's been on the market for 60 days tells you the seller is holding firm — for now.

List price vs. Zestimate gap

Calculate: (List price − Zestimate) ÷ Zestimate × 100

This shows how the seller is priced relative to Zillow's automated valuation model. It's imperfect — Zestimate has real error margins — but it's a useful reference point:

- 0–5% above Zestimate: Fairly priced. Little room unless DOM is high.

- 5–15% above: Seller has priced in negotiation room. You have leverage, especially with growing DOM.

- 15%+ above: Seller believes the property has premium value Zillow doesn't capture, or they're testing the market. Find out which before you bid.

- Below Zestimate: Motivated seller or property issue. Investigate and potentially move fast if everything checks out.

Combine all three signals. A listing at 45 DOM that dropped $25,000 and sits 10% above Zestimate is a very different negotiating position than a fresh listing at Zestimate. Treat them accordingly.

Set your offer range — all three numbers

Before you call your agent, determine three numbers. Know all of them before any conversation about submitting an offer starts.

- Maximum: The highest price you would pay and still be financially comfortable — based on your true monthly cost calculation from step 2, not your pre-approval limit. This is the ceiling you do not cross regardless of what happens in negotiation.

- Opening offer: Your starting bid, informed by the negotiation signals from step 3. In a low-DOM market at Zestimate pricing, opening below list price can cost you the deal. In a 60+ DOM market with a price history showing reductions, an opening offer 5–8% below list is reasonable.

- Walk-away price: The price above which you leave the negotiation. This is the most important number of the three, and almost nobody sets it in advance. When you're in the middle of a counteroffer conversation and emotionally invested, you will rationalize paying more than you should unless this number is already decided. Set it in writing before negotiations begin.

Your agent will tell you what they think the market supports. Listen to that input — they see comparable sales you might not. But the three numbers above come from your financial situation and your analysis, not from enthusiasm about the property.

Decide on contingencies before you're under pressure

Contingencies are clauses in your purchase agreement that give you the right to exit the contract (and recover your earnest money) if certain conditions aren't met. There are three that matter for most buyers:

Inspection contingency

Gives you the right to have the home professionally inspected and to negotiate repairs, request a price reduction, or walk away if serious issues are found. This is the most important protection a buyer has. Waiving it means you're buying the home as-is — with no recourse if the inspector would have found a failed roof, foundation issues, or faulty electrical.

Financing contingency

Protects you if your mortgage falls through after your offer is accepted. If you've been pre-approved, this rarely becomes an issue — but circumstances change. If you waive this and your loan is denied, you lose your earnest money deposit (typically 1–3% of the purchase price).

Appraisal contingency

Protects you if the home appraises below the agreed purchase price. Lenders will only loan based on the appraised value — so if you agreed to pay $600,000 and the appraisal comes in at $570,000, you either need to make up the $30,000 in cash, renegotiate the price, or walk away. Without an appraisal contingency, you can't walk away and keep your earnest money.

The decision on contingencies should be made in advance, not in response to a seller's counteroffer. Know your position before the pressure starts.

Submit the offer

Once you've completed steps 1–5, submitting the offer is straightforward. Here's how the process works:

- Communicate your terms to your agent: Your offer price, contingencies, proposed closing timeline, and any other terms (furniture included, seller rent-back, etc.). Your agent uses this to draft the formal purchase agreement.

- Agent prepares and submits the purchase agreement: This is the legally binding document. Your agent drafts it using the standard contract form for your state, attaches your pre-approval letter, and submits it to the seller's agent.

- Earnest money deposit: Most offers require earnest money — typically 1–3% of the purchase price — deposited into escrow within 24–72 hours of an accepted offer. This demonstrates you're serious. If you back out without a contingency reason, you forfeit it.

- Wait for the response: Sellers typically respond within 24–72 hours. They'll accept, reject, or issue a counteroffer. If they counter, you're in negotiation — and this is why your walk-away number from step 4 matters.

A few things worth knowing about the response window: sellers are not obligated to respond within any particular timeframe unless your offer specifies an expiration. Most agents include a 24–48 hour offer expiration as standard — it creates urgency without being unreasonable. If the seller doesn't respond in time, you can extend or move on.

If you receive a counteroffer, don't respond immediately. Take time to evaluate it against your walk-away number and the true monthly cost calculation. Counteroffers are designed to create urgency. The seller already took 24–72 hours to respond to you — you can take a few hours to respond to them.

Run your true monthly cost before you offer

HomePilot shows the full monthly cost breakdown — P&I, taxes, insurance, HOA, PMI, and maintenance — directly on every Zillow, Redfin, and Realtor.com listing. Know your real number before you schedule a tour, not after you're emotionally invested. Free for 5 properties/month.

Add HomePilot to Chrome — Free →5 free analyses/month · No credit card · Works on Zillow, Redfin & Realtor.com